How to Protect Your Money From Inflation in 2026 — Before It Eats Your Savings Alive

Inflation hit 3.8% in 2026 and it's quietly draining your savings. Here's exactly how to protect your money and come out ahead — practical tips for everyone.

FINANCIAL ADVICE

Financial Path Team

7/3/20269 min read

There's a thief operating in every economy right now, and it doesn't need a mask or a weapon. It works slowly, quietly, and most people don't even notice it until the damage is already done. That thief is inflation — and in 2026, it's back with renewed force.

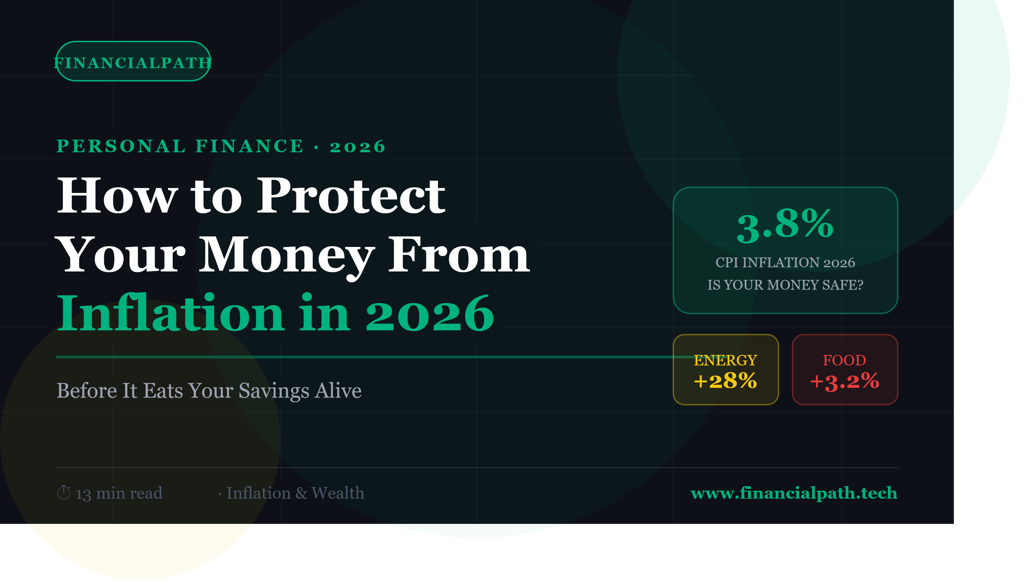

The U.S. Bureau of Labor Statistics recently reported that the Consumer Price Index rose 3.8% over the twelve months ending April 2026 — the sharpest annual increase since May 2023. Energy prices surged 28.4%, food costs climbed 3.2%, and shelter expenses are up another 3.3%. If you're reading this from Nigeria, Ghana, Kenya, or anywhere in sub-Saharan Africa, those numbers might even seem modest compared to what inflation looks like at home.

Knowing how to protect your money from inflation isn't optional anymore — it's one of the most urgent financial skills of this decade. And the good news is, once you understand what inflation actually does to your finances, protecting yourself is more straightforward than most people think.

Table of Contents

What Inflation Is Really Doing to Your Money Right Now

Why Keeping Cash Is the Most Expensive Mistake You Can Make

The Assets That Consistently Beat Inflation

How to Inflation-Proof Your Income

Practical Steps to Start Protecting Yourself This Week

Inflation in Emerging Markets — A Different Beast Entirely

Common Inflation Mistakes to Stop Making Immediately

Key Takeaways

1. What Inflation Is Really Doing to Your Money Right Now

Most people think of inflation as prices going up. That's accurate, but it misses the more important half of the story: inflation means your money is going down in value at the same time.

If you have ₦500,000 or $5,000 sitting in a savings account earning 2% interest annually, and inflation is running at 3.8%, your money is effectively losing 1.8% of its purchasing power every single year. The number in your account looks the same — or even grows slightly — while quietly buying less and less each month.

Over ten years at 3.8% inflation, that ₦500,000 today would need to grow to roughly ₦740,000 just to maintain the same purchasing power. If it only grew to ₦600,000 sitting in a low-interest savings account, you actually lost wealth — even though your balance increased.

💡 Tip — The Inflation Reality Check

Take your current savings balance. Multiply it by your local inflation rate as a decimal (e.g., 3.8% = 0.038). The result is how much purchasing power you are losing from that money every single year. For Nigerian readers dealing with inflation rates of 20%+, this calculation is even more sobering.

2. Why Keeping Cash Is the Most Expensive Mistake You Can Make

Here's something that feels counterintuitive: in an inflationary environment, holding large amounts of cash is one of the most financially destructive things you can do.

This isn't about being reckless with money. Emergency funds are still essential — three to six months of living expenses in a liquid, accessible account is still the right target, and that hasn't changed. The problem is holding excess cash beyond that buffer and calling it "safe."

Cash held in a low-interest account during high inflation isn't being preserved. It's being silently eroded. At Nigeria's current inflation levels, ₦1,000,000 today has the purchasing power of approximately ₦800,000 in twelve months — without a single naira leaving your account.

According to Experian's analysis of Federal Reserve data, total US household debt rose to $18.8 trillion in early 2026, driven by increases in mortgage, auto, and home equity balances — suggesting that many households are financing living costs rather than outpacing inflation with their savings. That is what happens when cash doesn't keep up. Morgan Stanley

The solution isn't to spend everything or avoid saving. It's to make sure your money is working rather than sitting still.

3. The Assets That Consistently Beat Inflation

Not all assets respond to inflation the same way. Some shrink in real value during inflationary periods. Others hold steady. A few actually tend to grow faster than inflation. Knowing which is which is where inflation protection begins.

Stocks and Equities

Over long periods — and this is the critical qualification — stock markets have historically delivered returns that outpace inflation. The global equity market's long-run inflation-adjusted average return sits around 5–7% annually, according to data tracked by Vanguard's market research.

Companies that sell goods and services can raise their prices alongside inflation, which tends to protect revenues and ultimately share values. This doesn't mean stocks are immune to inflation shocks — in the short term, rising inflation often pressures markets downward. But for money you don't need for five or more years, equities remain one of the most reliable inflation-beating vehicles available.

Real Estate

Property values and rental income have historically risen alongside or above inflation. When building costs go up and supply remains constrained — as is currently the case in most urban markets globally — property tends to appreciate in real terms.

In the Nigerian context, land and property in urban centres like Lagos, Abuja, and Port Harcourt have consistently maintained and often grown real value even through high-inflation periods. The limitation is liquidity — real estate requires significant capital and can't be quickly converted to cash if circumstances change.

Inflation-Linked Bonds

Some governments issue bonds whose returns are explicitly tied to inflation rates — Treasury Inflation-Protected Securities (TIPS) in the US, for example. These instruments guarantee that your return stays at or above the inflation rate, which makes them unique in their protection. The trade-off is lower returns in non-inflationary periods and limited availability in many emerging markets.

Investopedia's guide to TIPS provides a thorough breakdown for anyone interested in exploring this option through US markets.

Foreign Currency

For readers in Nigeria and other emerging markets with currencies experiencing significant devaluation, holding savings in stronger foreign currencies — US dollars, euros, or British pounds — provides a meaningful inflation hedge at the local level. Platforms like Grey, Wise, and Chipper Cash have made this more accessible than ever for African savers.

Gold and Commodities

Gold's reputation as an inflation hedge is long-established, though its performance in practice is mixed over shorter time horizons. It tends to perform best during periods of extreme economic uncertainty or currency crisis rather than mild inflation. Commodities more broadly — oil, agricultural products, metals — do tend to rise with inflation since they are the inputs that drive it.

4. How to Inflation-Proof Your Income

Protecting your savings is one half of the inflation equation. The other half — one that gets far less attention — is what inflation does to your income.

If your salary increases by 3% this year and inflation is running at 3.8%, you received a pay cut in real terms. Your purchasing power declined despite the raise. This is why income growth that keeps pace with or exceeds inflation is not a luxury — it's a financial necessity.

There are several ways to approach this:

Negotiate a cost-of-living adjustment. Many employees never ask. Framing a salary review conversation around inflation rates rather than personal performance is a legitimate and underused approach. If your employer knows the cost of living has risen 3.8% and you make that explicit, the conversation starts from a different place.

Build income streams in stronger currencies. This is where the FinancialPath Side Income page becomes directly relevant. Earning in dollars through freelancing, digital products, or remote work means your income automatically benefits from local currency weakness — which is one of the most practical inflation hedges available to anyone with marketable digital skills.

Grow skills that command premium rates. Inflation doesn't hit all professions equally. Specialists with skills in high demand — software development, data analysis, content creation, financial consulting — tend to see their market rates rise at or above inflation because demand for their work outpaces supply.

⚠️ Warning — The Salary Trap

Accepting a salary increase below the inflation rate without negotiating is quietly accepting a pay cut. Most employers will not automatically offer cost-of-living adjustments — you have to ask. Document the current inflation rate and bring it to the conversation with evidence.

5. Practical Steps to Start Protecting Yourself This Week

Understanding inflation is useful. Doing something about it is what actually matters. Here are concrete steps you can take starting now:

Step 1: Calculate your personal inflation exposure.

Look at your monthly budget. Which categories have risen most sharply in the last twelve months? Food, transport, and energy typically lead during inflationary periods. Knowing where your personal inflation rate is highest tells you where to focus.

Step 2: Audit your cash holdings.

How much money do you currently hold in low-interest savings accounts beyond your emergency fund? Any amount beyond three to six months of living expenses that's earning below the inflation rate is losing real value. That excess should be working harder.

Step 3: Move excess cash into inflation-beating assets.

Based on your time horizon and risk tolerance, begin moving excess savings into assets that historically outpace inflation. Index funds and ETFs are the most accessible starting point for most people. Our Compound Interest Calculator can show you exactly how different rates of return change your outcome over time — it's worth running your numbers.

Step 4: Open a foreign currency account if you're in an emerging market.

If you're in Nigeria or another high-inflation economy, opening a domiciliary account or signing up for a multi-currency wallet through Wise, Grey, or your bank's FX services is one of the most impactful moves available. Even converting a portion of savings monthly builds meaningful protection over time.

Step 5: Review your income against inflation.

Compare your income growth over the last twelve months against your local inflation rate. If you came out behind, that's your signal to either negotiate, build additional income, or both. The Income Planner tool on FinancialPath can help you map your current income sources and identify gaps.

Step 6: Increase investment contributions during downturns.

Counter-intuitively, inflationary periods that push markets down are often excellent times to increase investment contributions. You buy more units at lower prices, which means you benefit more when the inevitable recovery arrives. Dollar-cost averaging through volatility is one of the genuine advantages of consistent monthly investing.

6. Inflation in Emerging Markets — A Different Beast Entirely

Everything discussed above applies globally — but for readers in Nigeria, Ghana, Egypt, Kenya, and similar markets, inflation operates with an additional dimension that deserves its own section.

In many emerging markets, inflation isn't primarily driven by energy costs or supply chain disruptions (though these contribute). It's driven by currency devaluation — the local currency losing value against international benchmarks, which makes imported goods more expensive, which drives broader price increases across the economy.

Nigeria's naira, for example, has experienced significant devaluation over the past several years. This means that even if someone perfectly preserved their wealth in naira terms, they may have lost significant purchasing power relative to dollar-denominated goods and services — which increasingly describes most of the global economy.

💡 Tip — The Emerging Market Inflation Playbook

For readers in high-inflation or high-devaluation economies, the inflation protection strategy has an additional layer: currency diversification. Holding some savings in USD, EUR, or GBP is not just about investment returns — it's about maintaining purchasing power at a fundamental level. This is why building dollar-earning income streams is one of the most talked-about financial strategies among Nigerian and African professionals in 2026.

NerdWallet's inflation protection guide offers a solid global framework, though emerging market readers should weight the currency diversification aspect more heavily than the article's US-centric framing suggests.

7. Common Inflation Mistakes to Stop Making Immediately

A few patterns show up repeatedly in how people respond to inflation — and most of them make things worse rather than better:

Panic-selling investments when markets dip. Inflation often causes short-term market volatility. Selling investments during that volatility locks in losses and exits you from the market before the recovery. Inflation is a reason to stay invested in productive assets, not a reason to flee to cash.

Hoarding cash as a "safe" response. This feels safe. It isn't. As we've established, cash held in low-interest accounts during inflation is actively losing real value. Safety, in inflationary terms, means protecting purchasing power — not just the nominal number in your account.

Ignoring the inflation rate on debt. High-interest debt becomes more expensive in real terms when inflation erodes the purchasing power of your income. Conversely, fixed-rate debt becomes cheaper in real terms over time as inflation rises — which is why homeowners with fixed mortgages actually benefit from moderate inflation. Understanding this nuance changes how you think about debt prioritisation.

Waiting for inflation to "calm down" before investing. Inflation rarely announces when it's leaving. People who wait for perfect conditions to invest consistently miss the best periods for buying. Time in the market, across inflationary and deflationary periods alike, remains the most consistent predictor of investment outcomes.

Ignoring your biggest inflation hedge — your skills. The most inflation-resistant asset most people own is their ability to earn. Investing in skills that command higher rates — through courses, certifications, or deliberate practice — is inflation protection in the most practical sense possible.

Key Takeaways

Inflation at 3.8% (US) in 2026, and significantly higher across emerging markets, means your money is losing purchasing power every single day it sits still

Cash beyond your emergency fund in a low-interest account is not "safe" during inflation — it's silently losing real value

Stocks, real estate, inflation-linked bonds, foreign currency, and gold are the assets that historically provide inflation protection

For emerging market readers, currency diversification — holding savings in USD or EUR — is one of the most impactful inflation protection strategies available

Income must grow at or above the inflation rate to maintain real purchasing power — negotiate, build skills, or add income streams

Never panic-sell investments during inflation-driven market volatility — staying invested is almost always the right move

The Inflation Hedge page and Income Planner on FinancialPath are your next practical steps

Related Articles to Read Next on FinancialPath

How to Build Multiple Income Streams — Because earning more is the most direct response to inflation eroding your purchasing power

The Savings Habit That Beats Willpower Every Time — Your savings need to be working, not just sitting. This article tells you how to make that happen automatically

Small Investing Moves That Compound Into Something Real — The practical starting point for putting your money into inflation-beating assets without needing a large sum to begin

Inflation won't wait for you to get ready. The readers who come out ahead of it in 2026 and beyond are the ones who understand what it does, take deliberate steps to protect their income and savings, and don't let fear or inertia keep them holding cash while their purchasing power quietly disappears.

FinancialPath is built to help you take exactly those steps — with tools, calculators, and articles designed for real people at every income level. Explore the Compound Interest Calculator, the Debt Paydown Calculator, and the Inflation Hedge page — they're free, and each one is built to help you make better financial decisions starting today.

FinancialPath

Inflation-hedging wealth blueprints for emerging market builders.

RESOURCES

GET IN TOUCH

info@financialpath.tech

Abuja, Nigeria

Serving emerging markets worldwide

© 2026 FinancialPath-No-nonsense math for emerging market builders.

LOCALLY RELEVANT, GLOBALLY USEFUL